As you accrue a credit history, you create the financial trajectory of your life. But let's face it: it’s much easier to kill your credit score than it is to re-build it. Whether you damage your rating through ignorance or by simply making poor decisions, you're going to suffer the consequences.

Here are some of the most common ways to shoot your credit score in the foot:

1. Fail to monitor your credit reports and report errors

Equifax, Experian and TransUnion are the three major credit reporting agencies. They often contain mistakes in your history. It’s up to you to report errors and report changes co all three agencies.

2. Default on loans

Having an open floor plan led to an average 7.4% appreciation per year. Less desirable? Granite countertops (2.5% annual appreciation) and stainless steel appliances (3% annual appreciation)

3. Make late payments

Running up a history of making late payments on debt can crater your credit score. Some 35 percent of your score is based on payment history.

4. Carry huge balances

Big balances increase your credit utilization ratio—the total percentage of your usable credit limit—and warns lenders that you're a risk.

5. Open too many credit card accounts

If you're one of these consumers who snatches up handfuls of store credit cards during the holidays in order to obtain in-store offers, you might find as much as 30 points lopped off your score. Your would-be new lenders all ask for credit scores and your rating goes kerplunk. Yes, it's good for your credit to have a couple of cards chat you regularly use and pay down, but too many raises red flags.

6. Co-sign loans for your family members

As a co-signer, you assume co-responsibility for defaults and late payments by family members. If the car ar items purchased with the loans are re-possessed, welcome to a world of credit hurt.

7. Close credit card accounts

The lower your credit card utilization (credit used divided by available credit), the better your credit score. Closing credit accounts lowers the total amount of credit available to you and can negatively impact your credit utilization ratio. It's a quick way to max out your existing credit and put you in a category of higher loan interest rates going forward.

8. Miss “trivial” details

You forgot to pay a few parking tickets, so what? You moved to a new town without paying off your library fines, or you misplaced the closing utility bill. Not important? Yes they are. If these and other loose end items are sent to collections, you can watch your scores plummet, And don't forget any bank accounts you've depleted, but haven't closed. If the bank applies penalties on delinquent account fees or sends the account to collections, your credit scores can take a surprise hit of ten or 20 quick points.

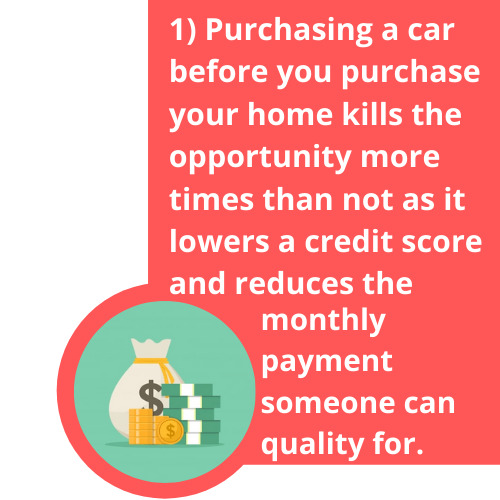

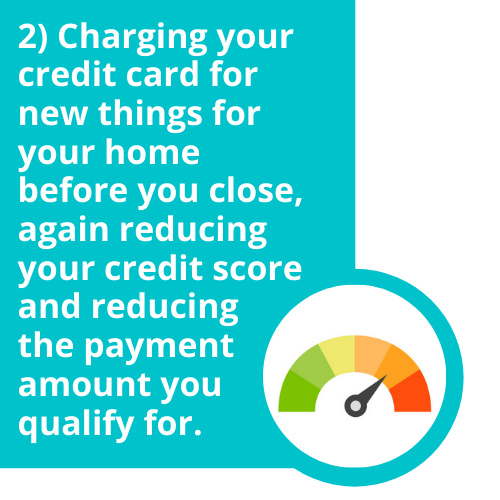

Top mistakes buyer made as they prepare to purchase a home

We have seen this multiple times over the years, so be mindful and don't make these mistakes which creates a lot of heartache.

For more information on how to build your credit score, read the articles below.

(Click the images to read)

If you have any questions or comments you would like answered in next month's newsletter, email me at [email protected] and they will be included in the market update. OR if you would like more information on our unique systems and programs, call us at 206-391-7766 or visit our website www.GeorgeMoorhead.com

©2020. All rights reserved